Inflation is back, IMF Growth forecasts are bearish

As another year-end reporting cycle approaches for investment entities, we face into significant headwinds for businesses and economies. Few are insulated from the present challenges and for investment firms many of these factors will manifest in the valuation process across portfolio holdings.

Global macro-economic factors that will influence the valuation process include:

- rising levels of inflation.

- increases in interest rates.

- commodity and energy supply shortages, rising costs; and,

- increased market volatility.

Over the past 12 months we have witnessed significant declines across both equity and debt markets. What has been observed across public markets will undoubtably factor into the valuation process for privately traded investments. We would expect such factors to manifest in lower market multiples, a consequence of which will lead to lower levels of IPO activity, which in turn may impact exit events planned for and factored into portfolio level valuations.

In these testing market conditions the risks associated with the valuation of financial assets and liabilities will need to be carefully managed and overseen. With this in mind we have identified some of the key challenges that managers and their boards of directors will face over the coming months.

1. Private Equity

Sensitive to Market Multiples, Cost Increases, Volatility, Cost of Capital assumptions.

The most commonly applied valuation technique for private equity instruments is the Market Approach, where enterprise valuation models or recent market transactions are used as a proxy for fair value. For portfolio companies valued using models, careful consideration must be given to the calibration of such models, taking into account a contracting market. The combination of rising levels of inflation and interest rate costs will lead to higher levels of economic uncertainty. Additionally, valuation models that rely on forecast periods that go beyond the next 12 months must be examined closely and challenged for overly optimistic revenue and/or EBITDA projections.

Assumptions made and judgements applied relating to comparable guideline companies or transactions will be scrutinised more closely to assess not only the suitability of the selected multiples but also the geographic market and industry such companies principally trade in.

According to IPEV (International Private Equity & Venture Capital Valuation Guidelines):

- While accounting standards do not specify a hierarchy of valuation techniques, the use of multiple techniques should be considered.

- IFRS 13 states that “in some cases a single valuation technique will be appropriate, in other cases, multiple valuation techniques will be appropriate”.

- When multiple valuation techniques are used the results shall be evaluated considering the reasonableness of the range of values indicated by those results.

We recommended to our clients to utilise the market approach (and observable data) to the maximum in private equity valuations. As per IPEV, “income-based techniques may be helpful in corroborating Fair Value estimates determined using market-based techniques”. Using the Income / DCF methodology in isolation is not recommended as such models can be less reliable and highly sensitive to fewer market observable inputs.

2. Private Debt

Sensitive to Discount Rates, Yields, Inflation, Serviceability.

The Income approach is the most commonly applied valuation technique when valuing income yielding investment positions such as private debt. There is no hiding from the fact that when interest rates increase the value of debt (bonds) will go down.

For debt issued at floating rates, as rates increase consideration should be applied to assessing the credit profile of borrowers and their ability to continue to service their debt into the near future. Leverage analysis, interest coverage & cash-flow forecasts should be utilised to monitor such borrowers free cash flows whilst also taking into account possible changes in demand as a consequence of a changing economic times.

Where no default events are expected, the yield analysis takes centre stage. Yields need to be recalibrated between the origination date (or latest arm-length transaction date) and the reporting date to address the changing spreads observed on the markets, as well as risk-free rates dynamics.

Recalibration of spreads between the origination date and the valuation date should consider two main components:

- Spread adjustment associated with the overall market spreads movement for the related credit rating category of the instrument, and

- Spread adjustment associated with the deterioration of the credit quality of the instrument since the latest arm-length transaction.

In instances where default events are a possibility it is recommended to use waterfall analysis to assess the expected recovery on the debt instrument, the timelines of expected recovery and the appropriate discount rates to price the defaulting instruments.

3. When Cost is the chosen proxy for Fair Value

Sensitive to IPO Markets, Rising Cost, Debt Serviceability, Uncertain Markets.

According to IPEV “where the Investment being valued was itself made recently; its cost may provide a good starting point for estimating Fair Value”. What defines “recently” is up for debate but with the passage of time and taking consideration for the prevailing market uncertainty it is recommended as good practice to identify additional supports to assist in validating a cost-based valuation.

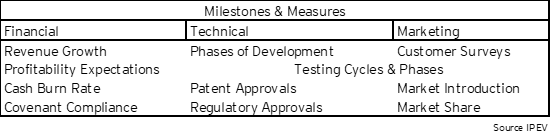

Such supports will tend to be qualitative, including scenario-based methods and identifying milestones (see table below).

The IPO Market is underperforming based on the prior year. Global IPO volumes are down circa 50%. In situations where investors had assumed IPO exits at the outset may need to sit-tight. Valuations will need to be more robust – the price paid for the investment may not remain as the value of the investment

“Price is what you pay; value is what you get.”

4. Valuation methodologies, policies & procedures

Managers should review their current portfolio composition with the specific objective of identifying gaps where the valuation approach for specific portfolio holdings is challenged as a result of current market conditions.

The choice of valuation methodology may then need to be amended to better reflect (a) the true valuation and (b) the current market dynamics and related sensitivities.

With a gap analysis completed, managers, together with their valuation functions and committees should then determine:

- Whether the entities valuation methodologies, policies and procedures provide the valuation team with enough guidance on how to operate across each of the investment types that the fund holds; and

- Whether amendments may be required to address challenges associated with particular investment types caused by factors referenced above. This relates to qualitative and quantitative aspects – critical to identifying changes in a portfolio company’s fundamentals.

Any changes to an entity’s valuation method, policy or processes should be approved by the appropriate valuation committee or governance structure in place within an asset manager. Consideration should also be given as to whether any such change constitutes a material event of which would need to be disclosed to investors in accordance with AIFMD.

Summary

While the Covid-19 Pandemic might now be in the rear-view mirror, a new set of risks and challenges have presented themselves across the global investment community. The ongoing war in Ukraine has been a catalyst for volatility, higher inflation & interest rates, energy supply issues, uncertain public & private equity markets and lower market multiples.

The opportunity and task at hand is for market participants to revisit their valuation and risk-management procedures and controls to successfully navigate these ongoing turbulent times.

References:

Global IPO market continues to plummet as Q3 draws to a close | EY – Global

Inflation on the rise – quo vadis, business valuation? (luxtimes.lu)

IPEV Valuation Guidelines – December 2018.pdf (privateequityvaluation.com)

Contact Us

If you would like more information on how EY's team of experts can help, please reach out today.