- Standardised Approach to Credit Risk

- IRB (Internal Ratings Based Approach)

- FRTB (Fundamental Review of Trading Book)

- Capital Output Floor

- Operational Risk

- CVA (Credit Valuation Adjustment)

- Legislation Timelines

- What are the key changes to this legislation?

- What should financial institutions be doing at this stage?

- How can EY help

- Contact us

Basel III is an internationally agreed set of measures developed by the Basel Committee on Banking Supervision in response to the financial crisis of 2007-09.

The European Commission’s (EC) legislative Banking Package (including CRDVI and CRRIII) was published on the 27th of October 2021. This was the first step in the finalisation of the Basel standards in the EU. The Council of the European Union and European Parliament have subsequently published their own amendments to the existing CRR and CRD legislation and trilogue discussions are underway to determine the content of the final changes to be published in the European Union Official Journal.

This Banking Package (CRRIII and CRDVI) is due to be implemented on the 1st of January 2025.

This will be at the forefront of the CFO agenda across the Financial Services sector in the coming years. We’ve pulled together a summary of the legislation, highlighting the recent changes and additions, looking also at what firms should be thinking about right now to meet the deadline.

![]()

Standardised Approach to Credit Risk

- The revised Basel rules introduce a number of changes on determining how institutions will determine the exposure value of off-balance sheet items and commitment on these items

- Introduction of two new credit conversion factors (CCFs) of 40% and 10% respectively, thereby removing the 0% CCF and only allowing its application in certain exemptions

- Significant change to Real Estate exposures to increase the granularity with regard to inherent risk posed by different types of real estate based on (Acquisition, Development and Construction) ADC and non-ADC e.g.; introduction of new IPRE and non-IPRE classifications.

- Exposures to corporates now subject to more granular risk weightings based on external ratings

- Project finance, object finance and commodities finance exposure classes are introduced under specialised lending exposures, in line with the IRB approach

- Revised amendments to introduce a preferential risk-weight treatment of 45% for revolving retail exposures that meet a set of conditions of repayment

- New risk-weight multiplier requirements for unhedged retail and residential retail exposures to individuals where there is a currency mismatch between the currency of denomination of the loan and that of the obligor’s source of income

- Revised risk weights for Equity exposures; like less risky assigned with 250% and longer term and speculative investments with 400%

IRB (Internal Ratings Based Approach)

- The financial crisis highlighted important deficiencies in the existing IRB approaches. The new proposals aim to address issues such as the wide variation in capital requirements across institutions, which hinders the comparability of ratios

- Amendments introduced limit the exposure classes for which internal models can be used to calculate own funds requirements for credit risk

- There is a restriction in the use of Advanced IRB for certain exposure types (Banks and other financial institutions, large and mid-sized corporates)

- The IRB approach is no longer available for equity exposures

- Input floors applicable to corporate exposures will apply in the same manner to exposures belonging to public sector entities (PSEs) and regional government and local authorities (RGLAs)

- Introduction of minimum values for institutions’ own estimates of IRB parameters used as inputs for the calculation of RWAs

- Scaling factor of 1.06 in calculation of Risk Weights removed

- Removal of the double default method applicable to some guaranteed exposures, leaving only one general formula for the calculation of risk weights

- Revised scope and calculation for own estimates of credit conversion factors

FRTB (Fundamental Review of Trading Book)

- Revised FRTB standards introduced and implementation of binding capital requirements under FRTB framework to replace current market risk framework

- Clarity provided on the definition of trading desk

- Revision of criteria used to assign positions to the trading book and non-trading book (banking book)

- Further specifications provided on conditions used for reclassifying an instrument between the two books

- Amendments to clarify the treatment of foreign exchange vega risk factors, and adjusted formula for vega risk sensitivities

- Modifications to introduce a lower risk weight for the commodity delta risk factor related to carbon trading emissions

- Replacement of current Internal Model Approach (IMA) by the Alternative Internal Model Approach (A-IMA)

- Further clarity provided on the conditions that institutions must comply with in order to be granted permission to use the A-IMA for the calculation of own funds requirements for market risk

- Amendment to clarify the value of correlation parameters

- Clarity provided on responsibilities of the risk control unit and the validation unit with respect to the risk management system

Capital Output Floor

- The output floor limits the capital benefit arising from the use of risk models across all risk types by establishing minimum risk weighted assets (RWAs) at 72.5% of the standardized (i.e., non-modelled) level

- The revised proposals aim to improve the reliability and comparability of capital ratios and reduce model risk overall

- Amendments aim to specify which Total Risk Exposure Amount (TREA) is to be used for the calculation of minimum own funds requirements

- The output floor is incorporated in CRR III and CRD VI at 72.5%. This is to be phased-in over 5 years to a level of 72.5%

- Although individual group entities below the EU parent will likely not be subject to the output floor, there is an approach specified to apportion floored RWAs at the consolidated level to subsidiary parent companies in each EU country. This will result in the impact of the consolidated floor being distributed across the countries in which an EU group operates

- The EC notes that the Pillar 2 Requirement and the systemic risk buffer can be used to address risks that are similar in nature to those addressed by the output floor and these may need to be amended to avoid double counting

- Acts as an additional back-stop to the risk-based approach to determining capital

Operational Risk

- Removal of the advanced measurement approach (AMA) and introducing a single non-model-based measurement approach (Standardised Measurement Approach, SMA)

- The new approach aims to tackle to weaknesses in previous approaches, while also improving the comparability of results across institutions

- The new approach is based on a Business Indicator Component (BIC) that the EC incorporates

- The calculation of the Business Indicator is based on an interest component, a financial component and a service component. A 3-year average is used for all components

- The EC approaches do not further consider historical operational losses. Hence, as a much anticipated development, the operational risk internal loss multiplier (ILM) element is effectively set at 1

- The Internal Loss Multiplier is based on historical loss data from the previous 10 years

- Capital requirements are calculated by multiplying the Business Indicator Component by the Internal Loss Multiplier

- Institutions will have to disclose historical loss data and maintain a loss data set

- Requirement to periodically review the quality of the loss data set

CVA (Credit Valuation Adjustment)

- Revised definition introduced to capture both the credit risk spread of an institution’s counterparty and the market risk of the portfolio of transactions traded with that counterparty

- New approaches were introduced for calculating own funds requirements for CVA risk (the standardised approach, basic approach, and simplified approach)

- Amendments provide clarity on which securities financing transactions are subject to the own funds requirements for CVA risk

- Under the standardised approach (SA-CVA), risk sensitivity depends on credit spreads and market risks factors, driven by values of derivatives, i.e. offers the highest level of risk sensitivity and more detailed calculations and inputs.

- Introduction of basic approach for calculating own funds requirements with simpler formulas and supervisory factors.

- Simplified approach, least complex method, for calculating the own funds requirements for CVA risk introduced, along with eligibility criteria for its use

- Amendments to reflect new requirements applicable to eligible hedges for the purposes of the own funds’ requirements for CVA risk

- New mandates for the EBA to develop guidelines to help identify excessive CVA risk

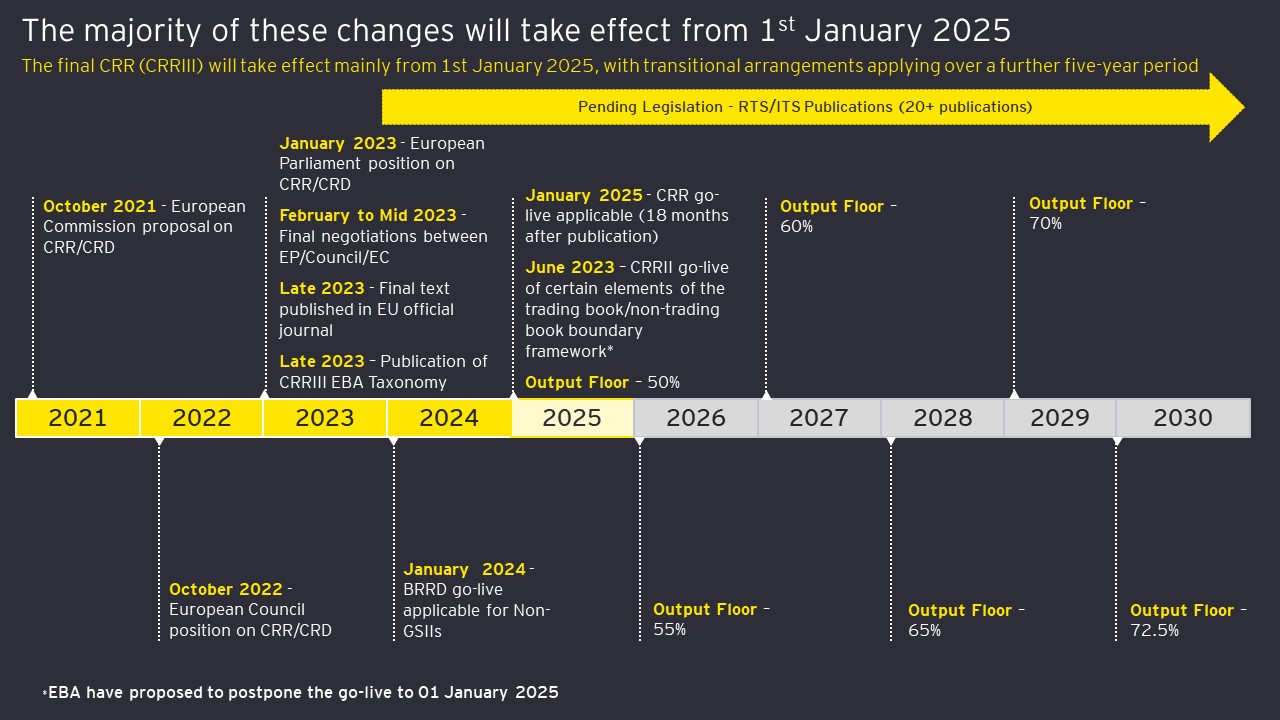

Legislation Timelines

The Banking Package (CRRIII and CRDVI) has an implementation date of 1st January 2025. We’ve charted out the key milestones in the below graphic.

What are the key changes to this legislation?

While the draft proposals from the Council, Commission and Parliament are broadly aligned, there are some key areas of divergence

Let’s look at a selection of these in more detail:

- Property Revaluation:

European Commission Proposal: allows for upward adjustment of property valuation beyond the value at origination to an upper limit of the average value over the previous three years for commercial real estate and six years for residential.

Council of the European Union Proposal: Broadly aligned to EC proposal however it increases the average value period to six years for both residential and commercial exposures.

European Parliament Proposal: Broadly aligned to EC proposal however it increases the average value period to four and eight years for residential and commercial exposures respectively. - Specialised Lending Exposures:

European Commission Proposal: Introduces 80% risk weight for unrated object finance and project finance exposures that meet the definition of ‘high quality’.

Council of the European Union Proposal: Removes preferential risk weight of 80% for ‘high quality’ object finance and project finance exposures and mandates an EBA report on the impact of implementing these lower risk weights

European Parliament Proposal: Maintains the 80% risk weight for object finance and project finance exposures deemed ‘high quality’ with some changes to the conditions required for project finance exposures to qualify as ‘high quality’ - Trade Finance

European Commission Proposal: Increases CCF for trade finance exposures to 50% and requires a 2.5 year maturity to be used where an institution has not received permission to calculate its own LGD estimates

Council of the European Union Proposal: Reintroduces the 20% CCF for technical guarantees and proposes the use of effective maturity for trade finance instruments as an alternative to the 2.5 year maturity proposed by the EC

European Parliament Proposal: Aligned to the Council’s proposal - Level of Capital Output Floor

European Commission Proposal: The capital output floor at a consolidated level but requires subsidiaries in separate member states to calculate their own output floor

Council of the European Union Proposal: The capital output floor will apply at an individual license level as well as a consolidated level but provides member states with the power to apply the output floor at a consolidated level only

European Parliament Position: Application at a consolidated level but with some allowances for host and consolidated home supervisors to apply output floor in separate member states to individual licenses

What should financial institutions be doing at this stage?

We have developed a three-phase framework for implementing the new CRDVI/CRRIII requirements which utilises our experience in regulatory change and considers the full institution wide impact of the new CRRIII & CRDVI requirements. Utilising this phased approach, and setting pre-defined outputs, will provide your organisation with a clear roadmap for successful regulatory implementation.

Ideally by now, banks should have completed the article interpretation and impact assessment highlighted.

How can EY help

Our team are highly experienced in working with clients on the requirements and business impacts of regulation. Working with us, we can offer you:

- A blended organisational chart where EY will take accountability but in a way that works with you. Our multi-competency team have the key skills to help you navigate each stage of the process e.g. Data and business analysts, subject matter resources, regulatory reporting testing and implementation experts

- Panel of EMEIA SMRs across a range of competencies on hand to provide support as and when required, with local leadership providing area focused expertise and acting as central point of contact with global team

- Support in starting and accelerating the journey, challenging our processes and ongoing identification of the next set of opportunities

- Invest in tools and methodologies for delivering and implementing process and system changes in response to changing regulatory requirements

- Facilitated sessions at one of EY’s innovation centres where we collaborate on use cases with the latest technology.

For more information, contact our team today

Contact Us

If you would like more information on how EY's team of experts can help, please reach out today.