Aided by ubiquitous mobile access and easy distribution through mobile app stores, FinTech companies and some progressive banks have started to make inroads with customers of traditional banks. This threatens banks’ vertically integrated and product-focused business model, which is not always suited for building or integrating innovative FinTech services.

Banks should explore the concept of platform-based banking. A banking platform establishes standards for third-party FinTech developers to build products and services on behalf of bank customers while allowing the banks to deliver a unified banking experience.

Digital economy innovations share a common factor: the platform-based business model. Through an intermediary platform, passengers can find drivers, visitors can find empty rooms, and in general, buyers can find sellers. Customers have embraced these platform-based businesses for reduced friction, lower prices and better service, along with the convenience of using mobile devices as the primary point of contact.

FinTechs are using rapid development methodologies on the latest technology stacks, launching products and services not yet offered by banks. Social networks allow FinTechs to target customers by geography or demographics, while app stores enable customers to enroll quickly and easily into new, personalized products and services that provide instant decisions and rapid transactions.

The banking industry has until now avoided the level of disruption seen in other industries, owing to a combination of:

Yet these are not insurmountable obstacles, especially when customers expect and demand higher levels of service and convenience. With mobile networks and platform-based business models, FinTechs can bypass the strengths of today’s banking industry.

In the traditional operating model, banks own and operate a vertically integrated value chain that stretches from production to sales, distribution and servicing. Even though banks can outsource various components, the overall cost structure remains relatively fixed.

The imminent threat of disintermediation makes the traditional operating model unsustainable. Using the rapid development tools available for mobile app deployment, FinTech companies can avoid entire expense categories involved with physical buildings and computing infrastructure.

The new entrants can also choose to compete in areas of strength with the highest profit margins, leaving low-margin, high-cost services to incumbent providers. They can design their new offerings from the ground up to be oriented toward self-service. The net result is that new competitors can challenge banks’ production costs while undercutting them elsewhere in the value chain.

Even though traditional banks have access to the same cloud-based technology stacks and rapid-development methodologies as FinTech innovators, they have been slower to take advantage of these approaches.

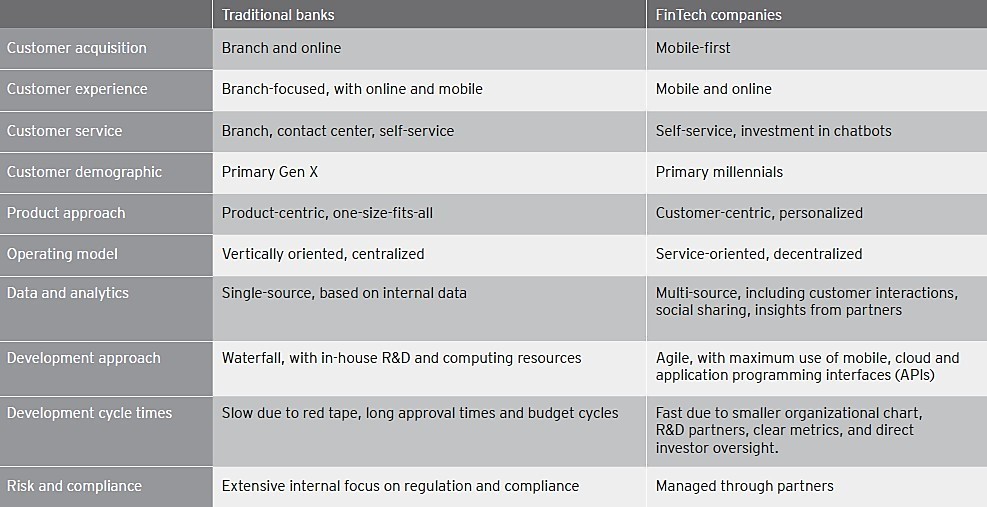

By contrast, venture-backed FinTech companies are built from the ground up to support the emerging customer base with the latest technology. Across several dimensions (see Figure A), FinTech companies are better-positioned to take advantage of deploying the latest technologies.

Figure A – Comparing traditional banks and FinTech companies

Traditional banks should seek to build an operating model that draws upon their strengths in terms of customer reach, regulatory expertise and branding.

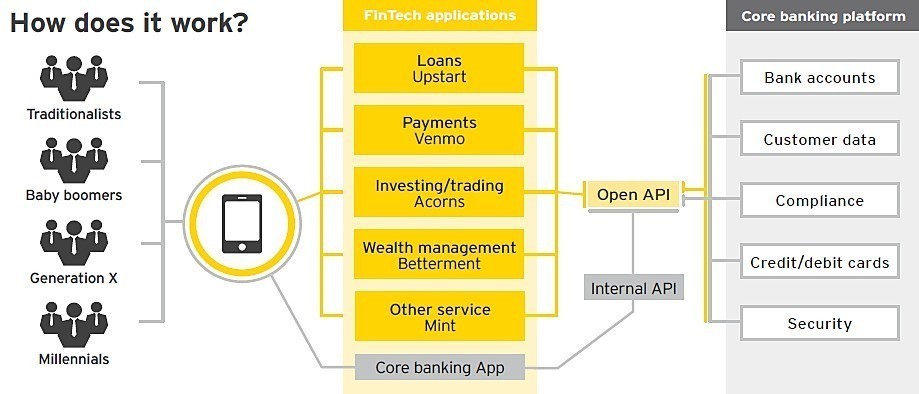

As translated to retail banking, a platform would intermediate between a broad range of financial products and services (including FinTech providers) and the mass market of retail customers.

A platform for financial transactions would need to establish plug-and-play standards enabling developers to build innovative products and services for consumers. The platform infrastructure would manage the secure exchange of data, oversee authentication and authorization, and ensure compliance with relevant regulations. Oversight and governance of a banking platform would ideally be managed using defined and shared standards among institutions working in federation with network operators and associations of FinTech companies.

Based on their knowledge of their own customers and markets, banks would use the full range of the platform’s capabilities to build omni-channel customer journeys that anticipate customers’ interactions across digital and physical environments.

The most challenging aspect of moving to a platform-based approach will be in managing the organizational change involved. The organizational aspects of platform-based banking include:

On the technology side, we recommend that banks use technology stacks and development methodologies similar to those used by FinTech companies. The technology steps to take to adopt platform-based banking include:

Figure B – Platform-based banking overview

Realizing the vision of platform-based banking will unlock the potential of technology in the financial services marketplace, and the benefits will accrue to FinTech companies, to retail customers and to the banks themselves:

Drawing upon their demonstrated strengths in regulatory compliance, information security and customer trust, banks can become valued partners and curators of financial platforms, enabling a new wave of diversified, innovation led revenue streams to support customer acquisition, retention, wallet-share growth and profitable revenue enhancement.

This article was originally published in The Alwin Club