1. Snapshot – what you need to know

- Under new Irish tax rules, Irish withholding tax may be imposed on certain interest, royalty and dividend payments.

- These new rules supersede any domestic exemptions you may have been availing of.

- The rules only apply to payments to “associated entities” in certain zero tax jurisdictions or jurisdictions on the EU non-cooperative list.

- While many structures should not be impacted by the rules, you will need to be able to confirm that you have no payments in scope (for audit purposes and ultimately in the context of filing the tax returns with Revenue).

The following sections of this alert include more details on the background to the rules and how they operate in practice.

2. Background

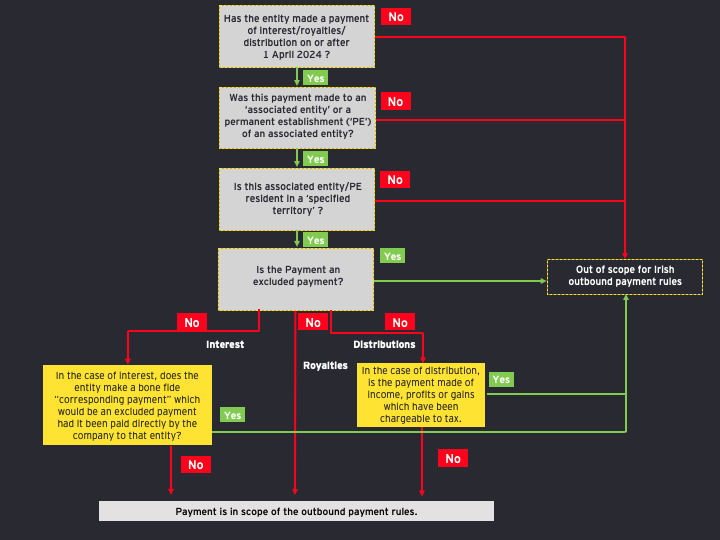

Finance (No.2) Act 2023 (‘The Act’) contained new defensive measures on outbound payments of interest, royalties, and the making of a distribution to an “associated entity” resident in a “specified territory” (or an associated entity’s permanent establishment situated in a specified territory). The new measures apply withholding tax, or disapply existing domestic withholding tax exemptions, on “in-scope” payments. The legislation applies to payments made by a company on or after 1 April 2024. Where the payment relates to arrangements in place on or before 19 October 2023, the rules will only apply to payments made on or after 1 January 2025. Irish Revenue issued guidance (“the Guidance”) in March 2024 which provides some helpful examples on how the rules are expected to operate in practice.

In our view, the rules should not generally impact significantly on many structured finance arrangements involving widely held funds but may impact on other investment structures. All structures involving payments from Ireland to a “specified territory” will need to be reviewed in detail in the context of these new rules.

3. Flowchart – The Basics

4. Key Definitions

As noted above, certain payments to “associated entities” resident in “specified territories” (or their permanent establishments in such territories) are in scope. See below commentary on how these terms are defined for the purposes of the rules.

(i) Associated Entity

The legislation provides that two entities will be associated where one entity is directly or indirectly entitled to more than 50% of the ownership rights, voting rights, assets, or profits of the other entity, or has “definite influence” in the management of the other entity. In addition, two entities will also be associated where there is a third entity in respect of which the first two mentioned entities are associated.

A company will have “definite influence” over another company:

…where one entity has the ability to participate, on the board of directors or equivalent governing body of the entity, in the financial and operating policy decisions of that entity, where that ability results, or could result, in the affairs of the entity being conducted in accordance with the wishes of the first mentioned entity.”

This is similar to the “significant influence” definition in the Hybrid-Mismatch rules, but unlike the “significant influence” definition, “definite influence” requires the ability to effectively control the affairs of the other entity.

(ii) Specified Territory

A specified territory is defined as “a territory, other than an EU or EEA Member State, which is a “listed territory or a zero-tax territory.” A “listed territory” is a territory on the EU list of non-cooperative jurisdictions. A “zero-tax territory” is a territory that, in respect of interest, royalties, or distributions receivable or received by an entity from sources outside that territory or derived by an entity from a source in that territory, imposes a tax at a nominal rate of zero per cent, or does not impose a tax that generally applies to such income.

It is helpfully confirmed in the Guidance that territories such as Hong Kong and Singapore which operate on a remittance or territorial basis of taxation are not, solely by reason of those features, considered a ‘zero-tax territory’. The Guidance also confirms that where a payment is made to a country which generally does not apply corporate income tax to companies but applies a corporate income tax rate in specific circumstances (such as to MNE’s with group revenue exceeding €750million), then this territory should still be regarded as a zero-tax territory for the purposes of these rules.

5. Interest

In general, Irish tax resident companies are required to deduct withholding tax on payments of yearly interest. However, there are various domestic exemptions from Irish interest withholding tax which can apply. Where applicable, the new outbound payments measures will disapply certain domestic withholding tax exemptions noted below:

- Interest payments made in respect of listed debt (Quoted Eurobond Exemption).

- Interest payments made in respect of wholesale debt instruments.

- All exemptions in the main withholding tax provision (s.246) which includes (but is not limited to):

- Interest paid in the ordinary course of a trade to a company which is resident in an EU state or tax treaty partner country where that jurisdiction generally taxes interest received.

- Interest paid by a Qualifying s.110 company to another person resident in a tax treaty partner jurisdiction.

The legislation also applies withholding tax to non-yearly interest payments (i.e., interest payments on loans with a term of less than 12 months) where such interest is within scope of the rules. Note – the provisions do not apply where no tax deduction is being taken for the interest payment (the rules are only applicable in the context of tax-deductible interest).

Quoted Eurobonds / Wholesale Debt

There is a specific exclusion from the rules where there is a payment of interest on a Quoted Eurobond (as defined in s.64) or wholesale debt instrument (as defined in s.246A) and where it is reasonable to consider that the payor of such interest is not, and should not, be aware that any portion of the interest is payable to an associated entity. This is an important exclusion from a practical perspective (further commentary in sector comments below in the context of structured finance).

Corresponding Payments

There is also an exclusion from the rules where there is a payment of interest to an associated entity resident in a specified territory and;

- the recipient of the interest makes an onward payment of a corresponding amount to another entity within 12 months of the end of the tax period;

- the corresponding amount would have been an “excluded payment” if it had been made directly to that entity (more on excluded payments below) and

- the payment was made for bona fide commercial purposes.

A corresponding amount means the portion of the interest payment received by an entity which is on-paid to another entity which is not resident in a specified territory. The Guidance clarifies that this exclusion will only apply to the immediate payment of a corresponding amount and would not apply to a multiple tier / multiple payment scenario.

Other Important Provisions – Interest

Section 8 below includes some other important general provisions which are relevant in the context of interest; in particular commentary on payments to transparent entities.

6. Royalties

The outbound payment rules operate by removing exemptions from withholding tax on royalties and applying a charge to income tax where an Irish company or an Irish branch of a non-resident company makes a tax-deductible royalty payment:

- to an associated entity resident in a specified territory or

- to an associated entity’s permanent establishment situated in a specified territory.

The rules will not apply where the payment is an “excluded payment” (more on excluded payments below).

7. Distributions

Where an Irish company makes a distribution to an associated entity that is tax resident in a specified territory, the existing domestic tax exemptions from Irish dividend withholding tax will not apply. However, where distributions are made out of income, profits or gains which have been chargeable, directly or indirectly, to domestic or foreign tax, then the outbound payment rules do not apply. This exclusion also applies where supplemental taxes such as CFC charge, GILTI tax and Pillar Two Top up Tax. The provisions shall not apply to distributions made out of foreign branch profits that are subject to foreign tax.

In addition, where the distribution is an “excluded payment”, the outbound payment rules do not apply.

8. Other Important Provisions

Excluded Payments

Certain payments and distributions are excluded from the scope of the outbound payment rules where they fall within the definition of an “excluded payment”. A payment will be an excluded payment where:

- The income, profits or gains arising from the payment is within the charge to a supplemental tax, foreign tax that is greater than 0% or an Irish tax. A supplemental tax includes taxes such as CFC charge, GILTI tax and Pillar Two Top up tax.

- The payment is made out of an amount of income, profits or gains which is within the charge to foreign tax at a rate above zero per cent.

Where the payment is to an entity in a territory other than a specified territory (or out of the profits of such entity), but the entity is exempted from tax which generally applies to profits income or gains in that territory, that payment will also be considered an excluded payment.

Payments to tax transparent entities

There are specific provisions in the rules dealing with payments to transparent entities. Where there is a payment to an entity or a permanent establishment and the payment is treated as arising or accruing to another entity or individual, the rules operate to treat the payment as if it had been made to the second mentioned entity or individual. In order for this treatment to apply, the payment must be considered to arise or accrue directly to the second entity or individual under the tax law of the first entity and the tax law of the second entity or individual.

The Guidance provides some helpful examples covering payments to tax transparent entities and how these are treated for the purpose of these rules. The examples also cover the interaction of these rules with the rules around corresponding payments noted above.

Anti-avoidance provision

The legislation contains an anti-avoidance provision which is applicable where an arrangement is entered into by any person, where it is reasonable to consider that the main purpose or one of the main purposes of the arrangement or any part of the arrangement is to avoid the new measures. Arrangements undertaken to eliminate existing payments to associated entities resident in specified territories (and that are not designed to merely circumvent the defensive measures) should not of themselves be subject to the anti-avoidance provisions.

Administration

Every company that makes a payment of interest or royalties or makes a distribution to an associated entity that is resident in a specified territory must return information in this regard in their corporation tax return. This reporting requirement applies even where the payment is considered an “excluded payment” described above.

9. Impact for Financial Services

See comments below on the new rules in turn by sector.

Structured Finance/Investment Funds

- Many s.110 companies will not be an ‘associated’ entity of the noteholder and consequently in those cases the rules should normally not be applicable. For example, public securitisation transactions should not be impacted given the Irish company should not generally be associated with the noteholder for this purpose.

- As noted above, the rules include a “knowledge-based” test, the intention of which is to disapply withholding tax under the new rules for payments of interest on a Quoted Eurobond or Wholesale Debt Instrument where it is reasonable to consider that the paying company is not, and should not be, aware that any portion of the interest payment is made to an “associated entity” as defined in the provisions.

- The withholding tax on dividends does not impact on distributions made by regulated funds such as an Irish Collective Asset-management Vehicle.

- The rules do not apply where the income / profits / gains in Ireland are within the charge to a foreign tax but the payment itself is disregarded for tax purposes in the payee jurisdiction. This could be relevant where the payee is disregarded for US tax purposes for example.

Banking

- The comments above regarding the use of s.110 entities will also be relevant for certain banking groups with s.110 entities.

- The structures and financing arrangements in banking groups will need to be reviewed in the context of these new measures on a case-by-case basis.

Insurance

- Insurance Groups with a presence in Bermuda would need to consider these new rules. Bermuda is introducing a Corporate Income Tax Rate of 15%, for accounting periods starting 1 January 2025, for Bermuda businesses that are part of multinational enterprise (MNE) groups with annual revenue of €750M or more.

- The Guidance states that where a territory only subjects entities to tax in certain circumstances, such a territory will still be considered a “zero tax territory”. However, the payment to such a territory may still qualify as an “excluded payment” (see comments above).

Aviation

- Aviation holding structures could be impacted with respect to upstream interest payments to intermediate holding companies and aggregator entities where they are located in specified territories.

- Where the aggregator entity is a partnership, we note there are effectively “look through” provisions for payments to an entity which is transparent (like a partnership) and some or all of that payment is treated as arising or accruing to a partner in another jurisdiction. In such cases it may be possible to regard the payment from Ireland as being made directly to the partners for this purpose, mitigating the impact where the partners are subject to tax on receipt. The Guidance provides helpful examples on payments to transparent entities and the interaction of same with the “corresponding payment” provisions.

We hope you found this alert helpful. If you’re interested in discussing any topics covered please feel free to reach out directly to the authors listed below.

Contact Us

If you would like more information on how EY's team of experts can help, please reach out today.