With the Corporate Sustainability Reporting Directive (CSRD) now in force, companies falling into scope will be required to provide disclosures on greenhouse gas (GHG) emissions in their value chain both from actors in the upstream and downstream value chain of a company. It covers a wide range of emissions such as those associated with the production of purchased goods and services, business travel, employee commuting, waste disposal, use of sold products and end-of-life treatment of sold products.

For organisations in the financial services sector, such as insurance firms, banks and asset managers, these will include financed emissions, namely GHG emissions associated with their lending, insurance and investment activities. By providing financial support to businesses, financial service organisations can enable a wide range of activities that contribute to GHG emissions. These include activities such as fossil fuel extraction, power generation, agriculture and transportation, among others.

The requirement for Scope 3 GHG reporting will impact SMEs in the value chain of larger companies in scope for the CSRD, as well as those which rely on financial service organisations such as banks and insurance firms for financial products and services. SMEs will therefore need to familiarise themselves with Scope 3 GHG emissions reporting requirements and keep abreast of regulatory requirements.

ESRS regulatory requirements for Scope 3 GHG emissions

Under the European Sustainability Reporting Standards (ESRS) which are mandated by the CSRD, Scope 3 GHG emissions reporting requirements are captured in the topical standard of ESRS E1 Climate Change. Specifically, under Disclosure Requirement (DR) E1-6, companies are required to provide disclosures on gross Scope 3 GHG emissions to provide an understanding of the GHG emissions that occur in its upstream and downstream value chain. As noted in DR E1-6, for many companies, it may very well be the case that Scope 3 GHG emissions form the main component of their GHG inventory.

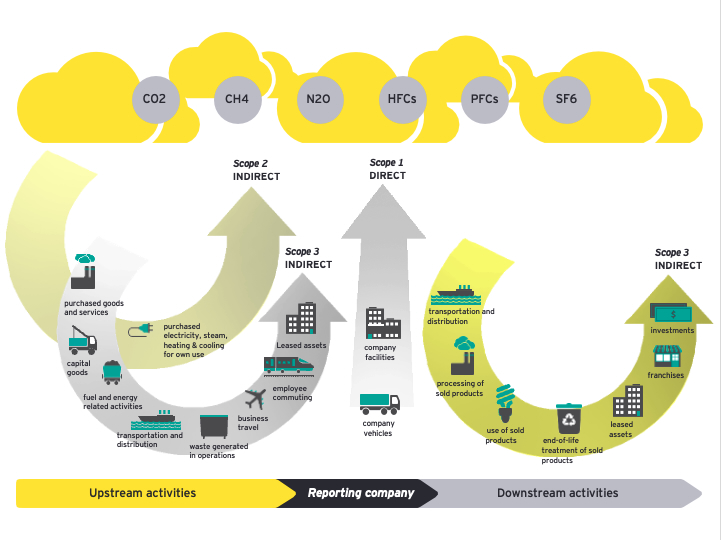

Figure 1: GHG emission categories [Source: GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard]

The ESRS mandates the use of the principles and provisions of the GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (Version 2011). Large companies that will be providing Scope 3 GHG emissions disclosures on their value chain emissions will be relying on this standard, thus making it an important one for SMEs to familiarise themselves with.

Even if SMEs are not captured as suppliers in the value chain of large companies, they will need to consider how their GHG emissions will impact their access to finance. Financed emissions are considered a form of Scope 3 GHG emissions under the GHG Protocol’s Corporate Value Chain (Scope 3) Accounting and Reporting Standard. Financial institutions have begun reevaluating their financial activities in sectors that are high GHG emitters. For example, in May this year, BNP Paribas and Credit Agricole – the second and third largest banks in Europe – decided that they would no longer underwrite bond issues for the oil and gas sector.

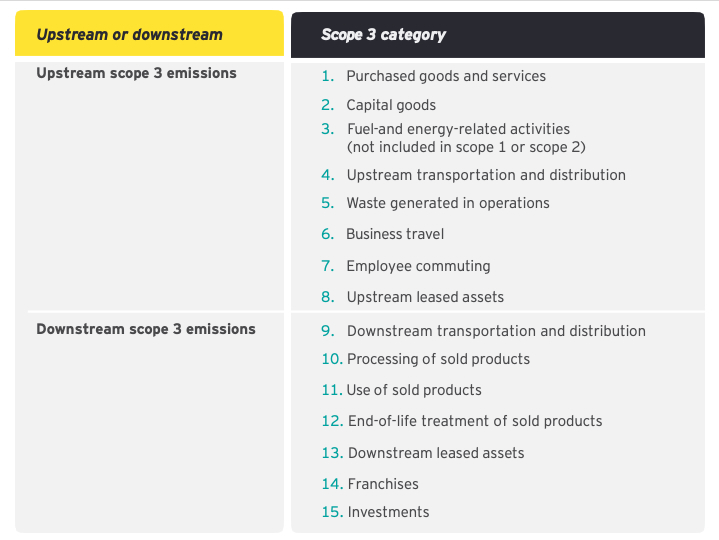

In relation to Scope 3 emissions, the ESRS requires companies to disclose the reporting boundaries considered, the calculation methods for estimating the GHG emissions and which calculation tools were applied. The GHG Protocol lists 15 categories in total, which can be distinguished as either upstream or downstream (See Figure 2) Scope 3 emissions. Companies do not have to report on all Scope 3 GHG categories, rather they are required to provide disclosures for each “significant Scope 3 GHG category”. Companies are also required to provide a list of Scope 3 GHG emissions categories included in and excluded from their GHG inventory, along with a justification for excluded Scope 3 categories.

Figure 2: List of Scope 3 GHG categories in the value chain [Source: GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard]

Applying the principles of the GHG Protocol

The accounting principles that underpin GHG accounting are similar to financial accounting and reporting. GHG accounting and reporting have to represent a faithful, true, and fair account of a company’s GHG emissions. The five principles which guide GHG accounting and reporting of the Scope 3 inventory are as follows:

- Relevance – the GHG inventory appropriately reflects the GHG emissions of the company and serves the decision-making needs of report users

- Completeness – the reporting accounts for all GHG emission sources and activities within the inventory boundary and justifies any exclusions

- Consistency – consistent methodologies are used to track performance over time

- Transparency – relevant issues are addressed in a factual and coherent manner, with a clear audit trail

- Accuracy – the quantification of GHG emissions is accurately conducted, and uncertainties are reduced as far as practicable

The reporting company will need to define its organisational boundary i.e. which operations are included and how emissions from each operation are consolidated. This will require the use of a consolidation approach, of which there are three under the GHG Protocol as follows:

- Equity share – accounts for GHG emissions from operations according to its share of equity in the operation

- Financial control – accounts for 100 percent of the GHG emissions over which it has financial control

- Operational control – accounts for 100 percent of the GHG emissions over which it has operational control

The GHG Protocol provides guidance on activities associated with each of these categories which are useful to provide more clarity. Further insight can be obtained from the European Financial Reporting Advisory Group (EFRAG) Value Chain Implementation Guidance released in May 2024 which provides an illustrative example in FAQ 6 on how calculations should be made for ESRS reporting purposes.

Challenges and benefits

With CSRD now live, there is significant demand for services related to Scope 3 GHG accounting and reporting. EY’s Climate Change and Sustainability Services (CCaSS) line have been working with clients – both large companies and SMEs – to help them decarbonise their operations and value chains and to reduce costs. We are also working with companies in-scope for CSRD, to prepare for their sustainability reporting under the ESRS.

SMEs can expect challenges as they begin putting in place processes to collect accurate and quality data for reporting purposes in line with the expectations of clients providing Scope 3 emissions reporting under the CSRD. Considering that sustainability reports require limited assurance, this needs to be factored into processes and systems that capture activity data required for the calculation of Scope 3 GHG emissions.

Notwithstanding the challenges, SMEs can also benefit from the exercise. SMEs that begin recording their GHG emissions will be able to use the information they obtain to find ways to reduce their emissions which in turn could result in reduced energy use and costs. There is also the potential for innovation as SMEs reassess their product and service portfolio to develop more environmentally friendly alternatives. All in all, while there may be some pain points as SMEs begin the process of recording their GHG emissions, in the longer term, they will benefit from the improvements they implement in their bid to reduce their carbon footprint.

This article was authored by Sheila Stanley, a Manager with EY Ireland’s Climate Change and Sustainability Services (CCASS) team servicing Financial Service Organisations. She is an experienced ACCA certified Integrated Reporting Practitioner who has developed numerous award-winning Integrated Reports, Sustainability Reports and TCFD Reports based on the Integrated Reporting Framework, GRI Standards, Sustainability Accounting Standards Board (SASB) and the TCFD Recommendations. As part of her engagement with CPA Ireland, she has conducted sustainability webinars, presented at the Irish Accountancy Conference, and developed content for the Sustainability Standards and ESG Challenges modules of CPA’s Sustainability Micro-credentials programme. You can view her LinkedIn profile on https://www.linkedin.com/in/sheila-stanley-b5447625/

- Greenhouse Gas Protocol: Corporate Value Chain (Scope 3) Accounting and Reporting Standard

- Greenhouse Gas Protocol: Technical Guidance for Calculating Scope 3 Emissions, Supplement to the Corporate Value Chain (Scope 3) Accounting & Reporting Standard

- ESRS Delegated Act

- EUR-Lex – 32021H2279 – EN – EUR-Lex (europa.eu)

- ey-global-carbon-accounting-standard-consultation.pdf

- PCAF launches the 2nd version of the Global GHG Accounting and Reporting Standard for the Financial Industry (carbonaccountingfinancials.com)

- Pair of major European banks backs away from oil and gas bond deals (ft.com)

Contact Us

If you would like more information on how EY's team of experts can help, please reach out today.