The five key drivers of digital ecosystems

1. Regulation

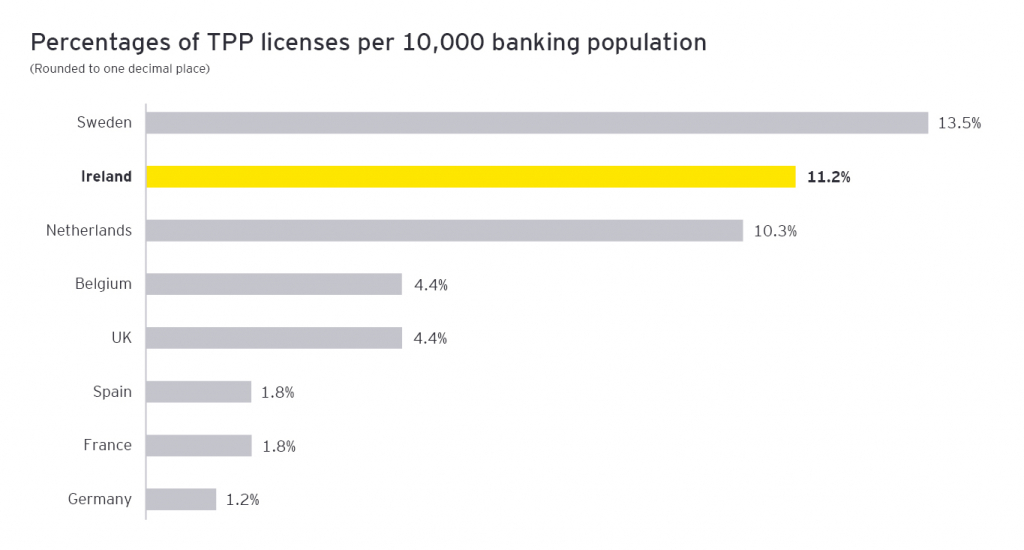

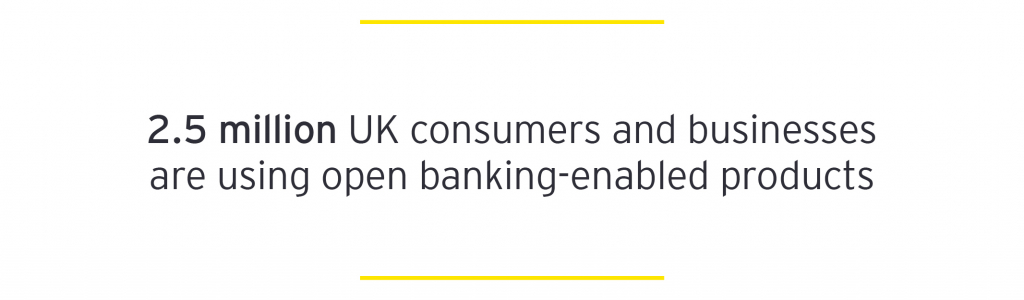

In Ireland and across Europe, the EBA’s Payment Services Directive 2 (open banking) legislation has levelled the playing field. Banks are now mandated to allow, with explicit consent, access to customer data and online payment capabilities through open API technology. According to the UK’s Open Banking Implementation Entity (OBIE), more than 2.5 million UK consumers and businesses are using open banking-enabled products, with hundreds of thousands of new customers being added to the ecosystem each month. Note: A similar body measuring open banking transactions does not exist in Ireland today.

2. Increased competition

With a lower barrier of access to the financial services market, FinTechs, BigTechs and challenger banks are leveraging their technological agility and superior digital customer experience to capture customers and investors. While digital banks like Revolut and N26 have signed up approximately 1.7 million Irish customers between them, few customers have fully migrated away from their pillar bank due to the limited services currently offered by these challengers – though that is not likely to remain true as such players are beginning to extend their offerings outside of payments products.

3. Increased digital and technology investment

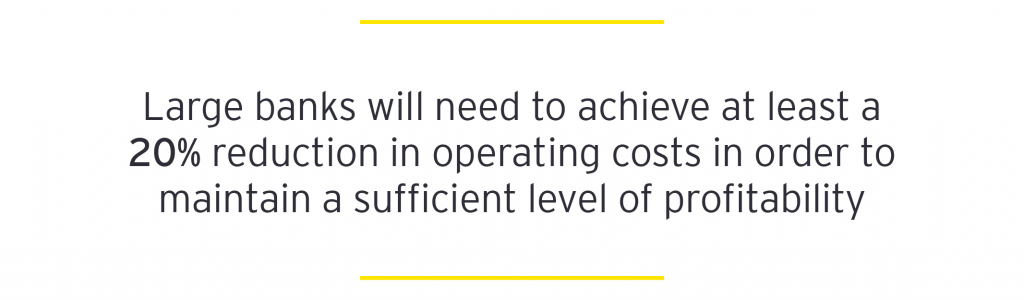

Banks are investing heavily in their technology systems and data. This drives down the cost to serve and creates a platform for new revenue streams. We estimate that large banks will need to achieve at least a 20-25% reduction in operating costs to maintain a sufficient level of profitability.

Globally and locally, banks are making major investor commitments to reduce costs, citing technology as the primary lever to achieve this. While regulatory change and legacy system renewal continue to consume the majority of spend, digital transformation and innovation budgets are increasing as the competitive threat resonates with shareholders.

4. Changing consumer behaviours and expectations

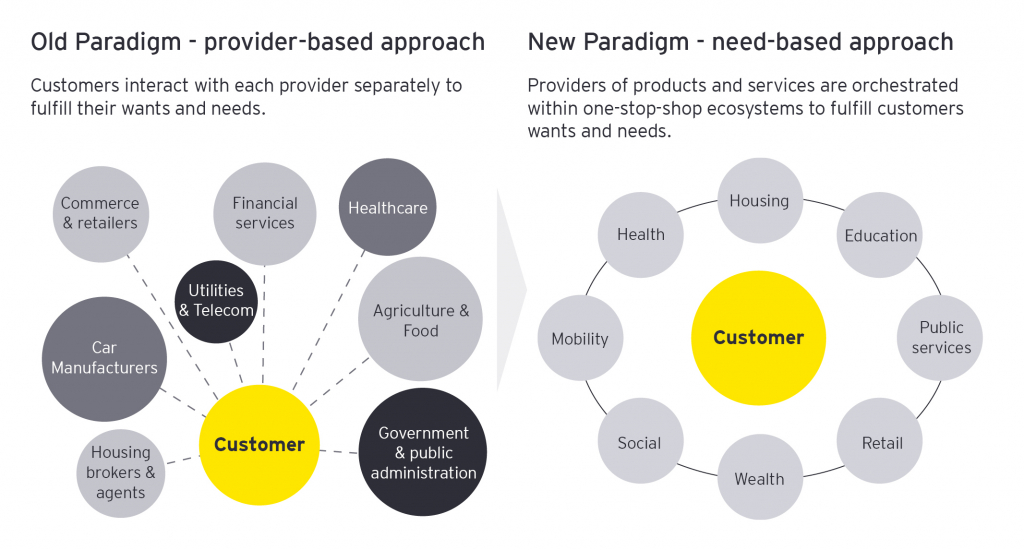

A change in paradigm is redefining the way consumers are serviced by breaking the silos of offerings and creating one-stop-shop ecosystems to fulfil customers wants and needs. In this new paradigm, Banks will succeed where they can embed their products and services at the point of need, e.g. embedded finance.

Based on the customer experience delivered by BigTechs such as Netflix and Spotify, consumers expect more personalisation, proactive services and connected omni-channel experiences from their bank. According to the EY Future Consumer Index, COVID-19 has accelerated digital adoption levels with 43% of global respondents saying the way they bank has changed during the crisis and 57% saying they had reduced their cash usage.

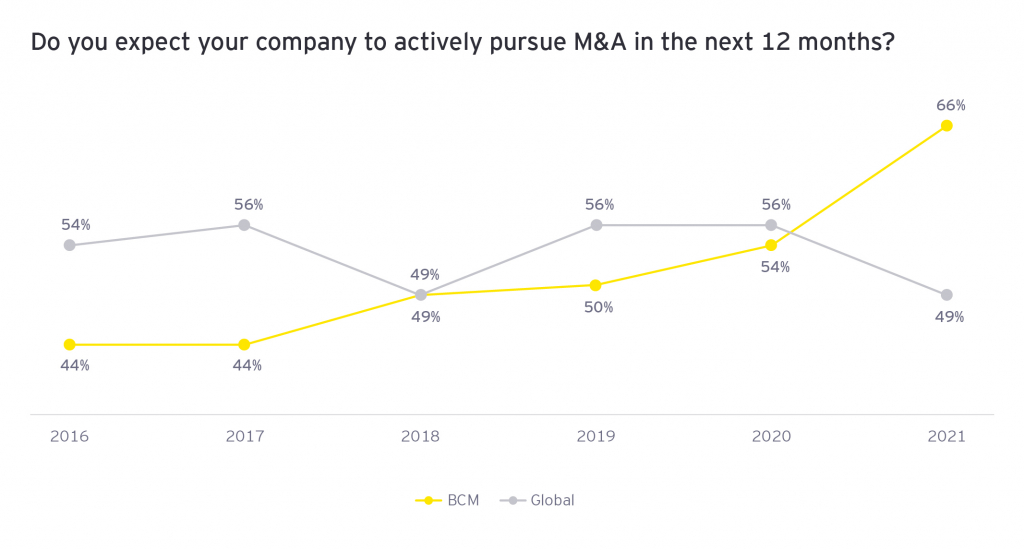

5. Partnership and acquisition appetite

According to the latest EY Global Capital Confidence Barometer (pdf), banks are increasingly focused on M&A and partnerships to accelerate inorganic transformation. 66% say they plan to actively pursue this over the next 12 months.

In Ireland, we see examples of this activity among some retail banks. How they will leverage these partnerships and acquisitions to build new digital products and services has yet to be seen, however. EY’s FinTech Adoption Index also shows Irish consumers embracing FinTech services at an unprecedented scale, with an adoption rate of 71% indicating that partnership-based services are likely to be well received.