According to the World Economic Forum (WEF) more than 50% of global GDP is moderately or highly dependent on ecosystem services. Ecosystem services refer to resources provided by nature that humans rely on. Examples of ecosystem services include food and water, the maintenance of habitats that support biodiversity, and natural areas such as parks that we use for recreation. According to the Taskforce on Nature-related Financial Disclosures (TNFD), the continued degradation of our planet’s ecosystem services represents an annual loss of approximately US$479 billion per year.

If left unabated and unmitigated, the damage to ecosystem services could result in significant negative financial impacts on industries that are highly dependent on them. These include sectors such as forestry, agriculture, food, beverages and tobacco, fishery and aquaculture, construction, water utilities and electricity.

Concerns surrounding nature-related sustainability issues are coming through in the policy and regulatory arena as seen through the imposition of nature-related sustainability reporting requirements and the proposal of new laws to protect natural resources and nature. As these come into play, SMEs will also need to consider how this will affect their businesses.

Nature-related dependencies that businesses rely on

According to the TNFD, there are four realms of nature that businesses and society depend on, namely freshwater, land, ocean and the atmosphere (See Figure 1), with people i.e. society, at the centre of it.

Figure 1: The four realms of nature [Source: TNFD]

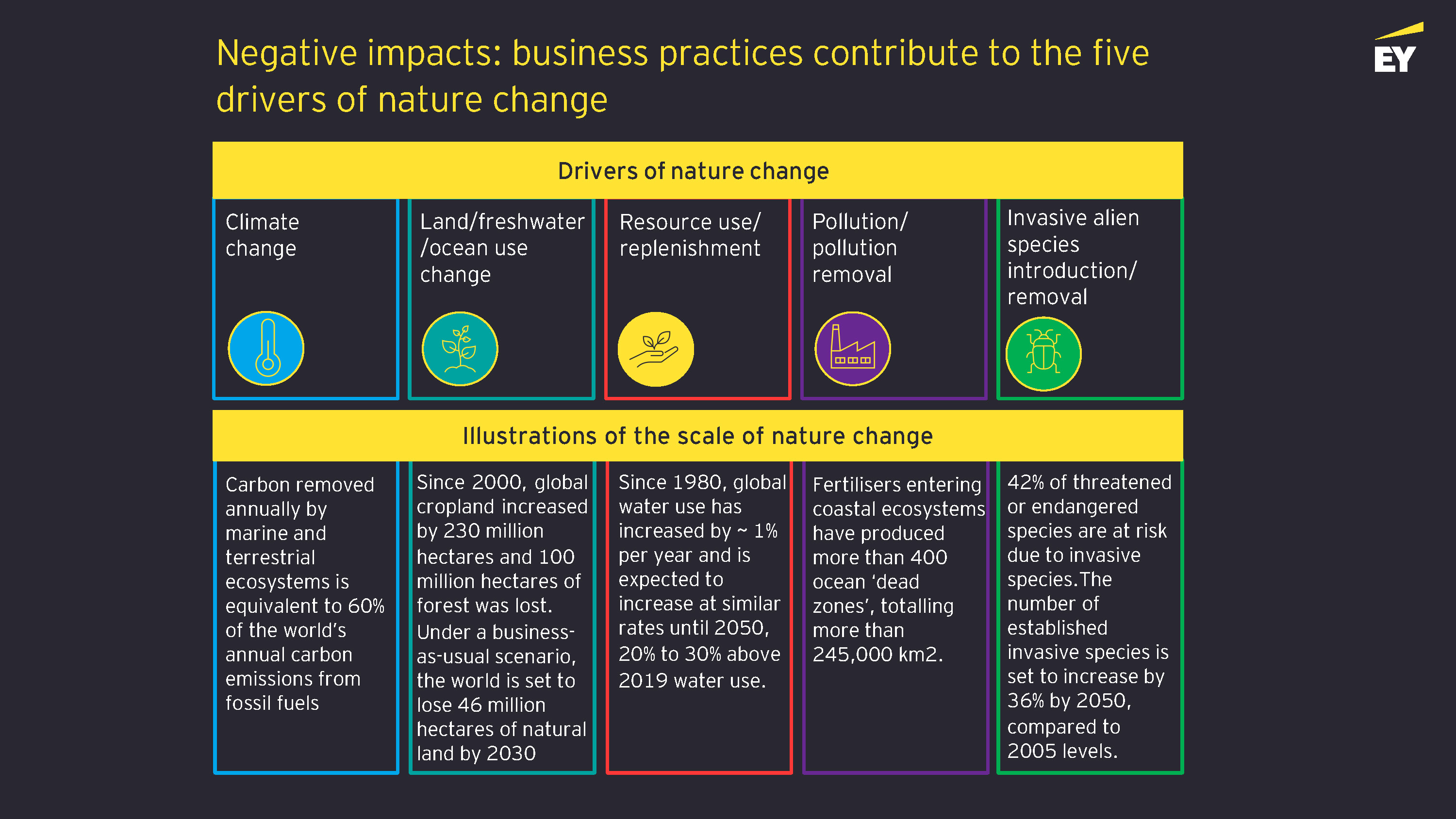

Examples of nature-related dependencies vary between sectors. For example, pharmaceutical companies develop prescription drugs based on molecules that can be found in plants while microchip manufacturers rely on vast quantities of water to maintain its manufacturing operations. These dependencies can give rise to negative impacts on nature cutting across the five areas of climate change, water use, resource use, pollution, and invasive alien species. (See Figure 2)

Figure 2: Examples of negative impacts businesses can have on nature [Source: TNFD]

Nature-related dependencies can also give rise to risks and opportunities. Let’s consider soil-related dependencies as an example. Scientific studies conducted on soil in the EU have found that soil degradation is increasing. An important ecosystem service that healthy soil provides is for food production, making it a nature-related dependency for the agriculture sector. A nature-related risk for the agriculture sector to consider is lower crop yields resulting from poor soil. To compensate for these nutrient deficiencies, farmers will need to invest in more fertilizers and pesticides to improve their yields, thus increasing their input costs. The increasing cost of agriculture will drive up the cost of food production. On the other hand, opportunities for the agriculture sector include implementing sustainable soil management and regenerating measures to improve soil health.

Nature-related sustainability reporting

An important sustainability reporting legislation requiring nature-related disclosures that SMEs need to be cognisant of is the Corporate Sustainability Reporting Directive (CSRD) which mandates sustainability disclosures under the European Sustainability Reporting Standards (ESRS). The specific ESRS topical standards that relate to nature are the environmental topics of E1 Climate Change, E2 Pollution, E3 Water and Marine Resources, E4 Biodiversity and Ecosystems and E5 Resource Use and Circular Economy. While it does not mandate it, the ESRS promotes the use of the TNFD’s Locate, Evaluate, Assess and Process (LEAP) approach as the means for a company reporting under the CSRD to identify and assess its nature-related impacts, risks and opportunities within its own operations and its value chain for the topical standards of E2 Pollution, E3 Water and Marine Resources, E4 Biodiversity and Ecosystems and E5 Resource Use and Circular Economy.

There is a two-year phase in for all disclosure requirements under E4 Biodiversity and Ecosystems for companies with less than 750 employees. While there are between one and three-year phase ins for certain disclosure requirements related to E2 Pollution, E3 Water and Marine Resources and E5 Resource Use and Circular Economy, the majority of disclosure requirements under these topical standards will be mandatory for the first cohort of companies reporting under the CSRD in 2025 based on their 2024 performance. Nature is currently being touted as the next climate change, with expectations that nature-related risks and opportunities will play a more prominent role when assessing business risks and opportunities.

Potential impacts on SMEs

With value chain reporting required under the CSRD, SMEs in the value chain of companies in-scope for CSRD reporting will find themselves impacted by these reporting requirements in the near-term future.

As larger companies begin reporting on nature-related disclosures under the CSRD, supply chain expectations will change in tandem. Larger companies will expect their SME suppliers in the value chain to step up on their nature-related commitments. Much like climate reporting has captured SMEs in the value chain as part of Scope 3 GHG emission reporting, nature-related reporting will require SMEs to provide their large clients/customers with information on nature-related matters.

Other impacts SMEs would need to consider is access to equity and debt finance and insurance. Financial institutions that are reporting under the CSRD will also be required to consider the nature-related dependencies of the businesses they lend to, invest in or insure. A recently published Global Survey conducted by the GARP Risk Institute on nature risk management across financial firms worldwide reveals that 46% of the Boards of financial institutions surveyed have oversight of nature-related risks and opportunities, while another 48% are working or intend to do so.

As an illustration, let’s consider the construction sector as a high impact sector. The construction sector uses cement from the cement manufacturing sector for its construction activities. The cement manufacturing sector, in turn, uses sand to manufacture cement. The WEF has noted that sand is the second most exploited natural resource in the world after water and demand for sand mining for construction materials has tripled in the past two decades. The high demand for sand is negatively impacting people and planet. For example, the United Nations Environment Programme (UNEP)’s 2019 Sand and Sustainability Report notes that marine sand dug up by the marine dredging industry is causing degradation to biodiversity and impacting the lives and livelihoods of coastal communities.

To achieve healthy soils, the EU has a proposed Directive on Soil Monitoring and Resilience in the pipeline which has classified sand as a protected soil. Ahead of the Directive coming into force, SMEs in the construction value chain should consider how this proposed Directive will impact them. Some specific impacts they need to consider would be how banks will integrate nature-related risks into their loan/financing portfolio assessments and how insurance firms reflect nature-related risks in their insurance premiums.

Preparing for the nature-related sustainability journey

SMEs that begin their nature-related sustainability journey now to align their business practices with nature positive practices and outcomes will find themselves developing a competitive advantage. Here are some ways that SMEs can get ahead of the curve in relation to nature-related sustainability considerations:

- Understand the ESRS reporting requirements for nature-related sustainability matters.

- Build their internal capability by identifying nature champions in their organisation to develop their nature-related knowledge and capabilities. There are a number of free resources available from organisations such as the TNFD for this purpose.

- Familiarize themselves with the nature-related dependencies of the business. They can begin by identifying potential impacts that the business may have on nature. The National Biodiversity Data Centre of Ireland has a mapping tool that SMEs can use to generate a biodiversity report for businesses located in Ireland.

- Begin having conversations with clients reporting under the ESRS to understand their ask in relation to the nature-related topical standards, and what information they would require from their value chain partners.

Watch this short video to hear Doreen Brennan, Director of Climate Change & Sustainability Services, and Sheila Stanley, Manager of Climate Change & Sustainability Services, discuss the lesser known topic of nature in ESG.

- The biodiversity business case: Companies need ecosystems | World Economic Forum (weforum.org)

- What Are Ecosystem Services, and How Do They Help Our Planet? (nationalgeographic.org)

- EU at COP15 global biodiversity conference – European Commission (europa.eu)

- Donor countries commit to increase biodiversity finance (europa.eu)

- Nature and biodiversity – European Commission (europa.eu)

- COMMISSION STAFF WORKING DOCUMENT EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT REPORT Accompanying the document Directive of the European Parliament and of the Council on Soil Monitoring and Resilience (Soil Monitoring Law) <eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52023SC0418>

- Nature restoration: Parliament adopts law to restore 20% of EU’s land and sea | News | European Parliament (europa.eu)

- Proposal for a Directive on Soil Monitoring and Resilience – European Commission (europa.eu)

- GARP Risk Institute, Global Survey of Nature Risk Management at Financial Firms 2024: A Discipline in its Infancy.

- TNFD in a box – TNFD

- Sand mining: how it impacts the environment and solutions | World Economic Forum (weforum.org)

- Proposal for a Directive on Soil Monitoring and Resilience – European Commission (europa.eu)

- National Biodiversity Data Centre – A Heritage Council Programme, Documenting Ireland’s Wildlife (biodiversityireland.ie)

This article was co-authored by Sheila Stanley. Sheila is a Manager with EY Ireland’s Climate Change and Sustainability Services (CCASS) team servicing Financial Service Organisations. She is an experienced ACCA certified Integrated Reporting Practitioner who has developed numerous award-winning Integrated Reports, Sustainability Reports and TCFD Reports based on the Integrated Reporting Framework, GRI Standards, Sustainability Accounting Standards Board (SASB) and the TCFD Recommendations. As part of her engagement with CPA Ireland, she has conducted sustainability webinars, presented at the Irish Accountancy Conference, and developed content for the Sustainability Standards and ESG Challenges modules of CPA’s Sustainability Micro-credentials programme. You can view her LinkedIn profile on https://www.linkedin.com/in/sheila-stanley-b5447625/.

Contact Us

If you would like more information on how EY's team of experts can help, please reach out today.