Since IFRS 9 came into effect on January 1st 2018, we have seen wide-scale transformation to meet the requirements of the standard – but banks are far from done.

First, the good news. So far, the impact on loan provisions has been less than expected, there is convergence in the application of multiple scenarios, and some of the best practices around stress testing are starting to crystallise – but challenges still remain.

The magnitude of change required was generally underestimated, and the longer-term impacts are still unclear. Embedding extensive additional risk and finance data, processes and controls into business as usual is no easy feat, and change programmes have extended longer than expected.

Banks continue to focus on stabilising risk and finance processes along with optimising their operating model. One specific focus is the number of working days it takes to complete calculations of expected credit losses and get through control and governance frameworks. The impact of IFRS 9 will not be limited to the transition period and first year of adoption, but will reach into 2019.

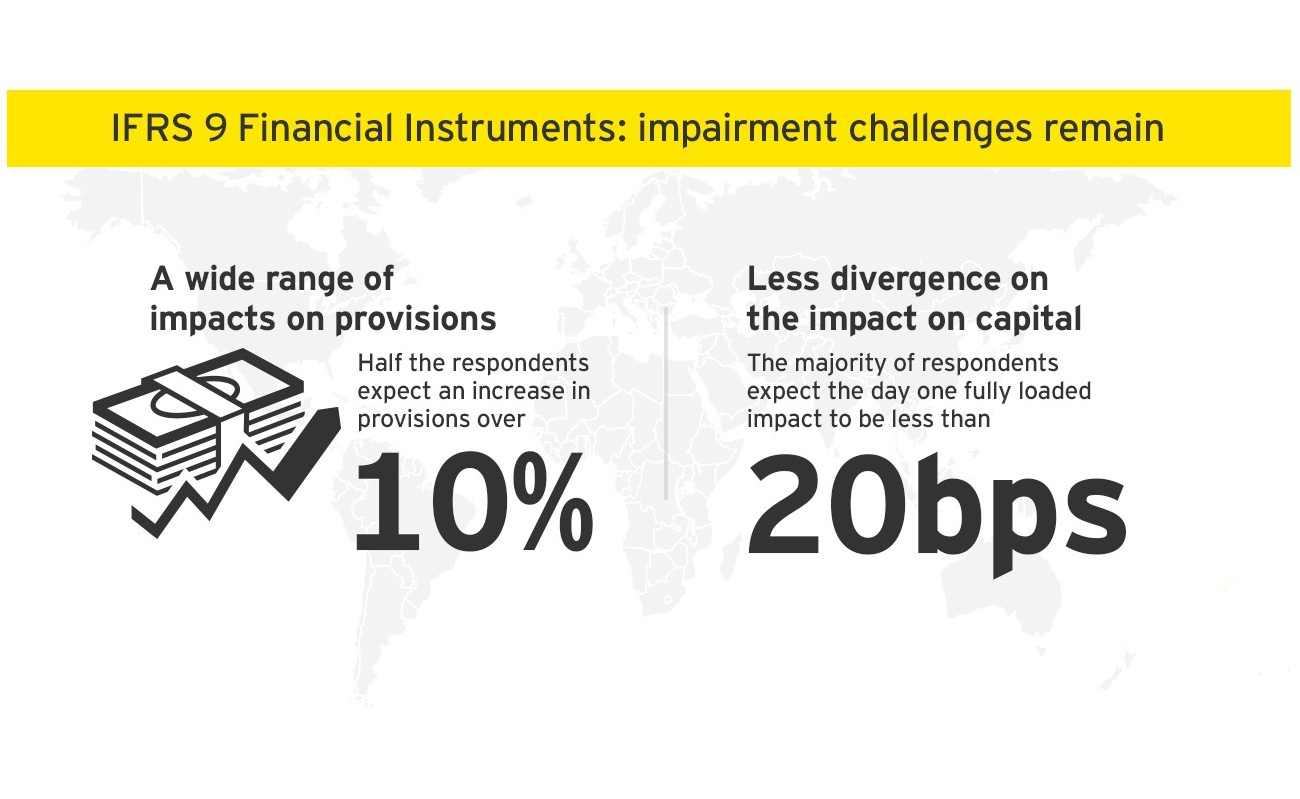

Our fourth annual IFRS impairment survey polled 20 major global banking institutions and compared the impact of, continued challenges and focus areas specific to impairment programmes. Key highlights include:

Our fourth annual IFRS impairment survey polled 20 major global banking institutions and compared the impact of, continued challenges and focus areas specific to impairment programmes. Key highlights include:

Download the report and explore our latest insights. If you have any questions relating to IFRS 9, including how your institution compares to the results in the survey, please do get in touch.