We are all aware of the importance of achieving a sustainable insurance finance and insurance sector. This year has seen a clear shift from voluntary participation in that ambition, to one that is increasingly mandatory. Those obligations are not just legal or regulatory: there is a social mandate, an expectation of the sector. The tools and supports to align to those mandates are available to industry players; the argument of uncertainty is falling away. It’s now a case of: What are you doing? And can you transparently demonstrate that you are adopting the sustainability mandate?

From my analysis, there are four key vectors driving the transition from voluntary to mandatory action on sustainability:

Vector 1 – Realising Net Zero

The achievement of Net Zero is an obligation for all of us. While not mandatory in a legal or regulatory sense, there is a clear social and moral obligation. This is being led from within the insurance sector, with early adopters and industry leaders coalescing under the banner of UN Net Zero Underwriting Alliance.

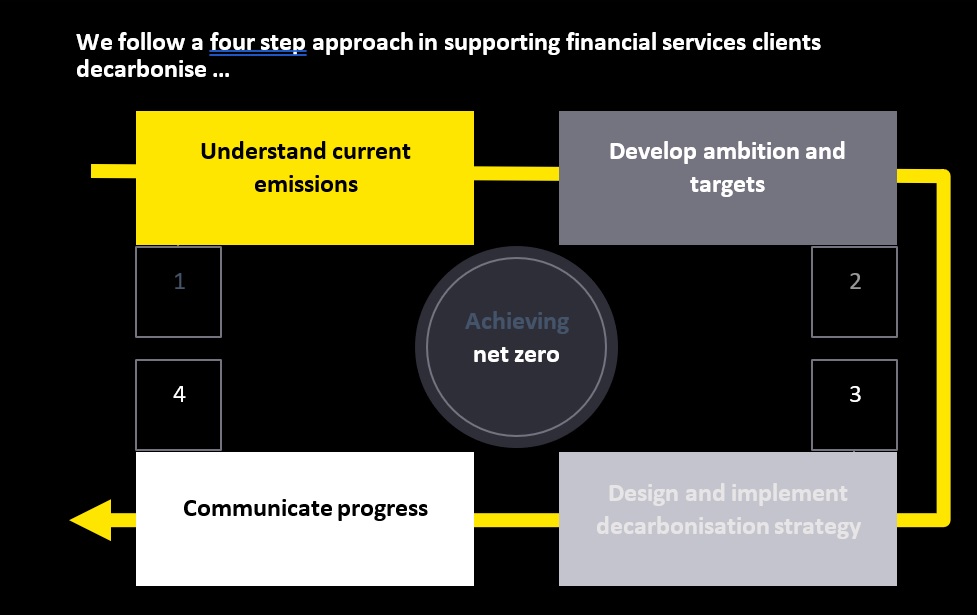

Setting aside the detail and complexity, we have identified a four step approach to decarbonisation.

Notwithstanding the simplicity of this model, it is important to appreciate the effort involved. We know that insurers and the FS sector as a whole can turn ambition into action. Organisations need to assess their current emissions, develop ambitions and targets, and have a clear plan to achieve them. Many organisations have had a desire to commit to action, but have been stymied as the challenges in measurement, monitoring and implementation present themselves. It is for those reasons a communication strategy becomes essential. It holds you accountable to your ambitions and commitments.

Vector 2 – The Reporting Mandate

The reporting mandate too is moving from voluntary to mandatory. This is the result of new regulatory reporting standards being enacted. They build on voluntary codes, such as the TCFD, that have been in operation for some years. Those who set accounting standards are supporting this move, as they seek to architect common standards and verifiable standards.

However, reporting is one of the most fluid areas of change, with a wide range of actors and proponents in place. It is also an area where there is still some way to go to confirm the European reporting frameworks. They are being deliberated under the Corporate Sustainability Reporting Directive, the successor to the Non-Financial Reporting Directive.

This diagram identifies some of the main actors and standards that are now moving to mandatory consideration for insurance companies and finance functions:

This in turn is driving the finance function in organisations to establish programs to deliver on their new reporting obligations. This comes at a time when those same functions are struggling with how to implement IFRS 17. The finance function can support both the reporting obligation and be a partner to the business on its sustainability journey, as the diagram below illustrates:

Vector 3 – The Prudential Mandate

The focus of climate risk action is to mitigate threats and adapt and build resilience to the future risk landscape. But there is now a focus on establishing the extent of current exposures, and the scenarios that may manifest under a range of different carbon pathways.

This forward-looking view has been consulted on and developed by EIOPA through their opinion on ORSA. It is key to the reassessment of the Natural Catastrophe scope and calibration under the Standard Formula. Each of these are key components of the EIOPA work plan in the last year.

We have a clearer view of the path of travel of EIOPA over the next three years as released this during their recent Annual Roundtable event: Sustainable finance roundtable: EIOPA announces its sustainable finance activities for the coming three years | Eiopa (europa.eu)

Among the anticipated developments is a move towards formalised assessment of sectoral risk. This would be achieved through a Risk Dashboard and assessments based on stress and scenario testing. This testing builds on prior methodology papers and will be exploratory in nature. This approach has been used already by the PRA in the UK. Exploration is not just to establish impact and exposure, but also to define the tools, data and capability required to perform such testing.

The move to embed climate risk into the risk function has moved from Voluntary to Mandatory. This has been effectively communicated by the CBI in their “Expectations” letter issued to all sectoral participants during November.

Vector 4 – A new strategy for Customers and Products

The customer and product mandate requires changes to both the end-to-end product and distribution process for retail and commercial coverage.

Without insurance, there will not be a transition. And without adaptation of insurance products and processes with sustainability in mind, insurance can’t deliver on its own mandate to achieve Net Zero.

There is a clear client demand for products that are more sustainable. However, the willingness to pay increased prices for ethical offerings is still not clear. Our consumer research still points to pricing as a key driver of purchasing decisions. Sustainability appears to be a secondary consideration at this time.

This pricing point came to a head in market consultation by EIOPA. They were exploring the suitability of building long-term non-life products that can anticipate future increasing non-life protection costs. The primary obstacle was the acknowledgement that existing protection gaps would increase if those products became more expensive.

That does not address the key consideration that such cover will become more expensive if climate change goes unchecked. In this regard, the first step is to ensure that products evolve to recognise the need for better adaptation to climate change. This needs to match how we consider direct insurance coverage to support transitions and promote the mitigation of climate change. We need to consider the extent of adaptative attributes for existing physical risk coverages so we can encourage adaptations.

We will see a global shift in financial flows that will be the norm over the coming decade. This will see insurance refocus its attention to support the transition of funds towards climate mitigation. It will also see flows being directed towards better resilience and adaptation.

Mobilising capital in a progressive and constructive way, that addresses the climate crisis, is an essential part of this process.

Another key aspect of this process is the Sustainable Finance Ireland agenda, which Insurance Ireland was a key contributor to. Establishing Ireland as a centre for sustainable finance is a critical and necessary step forward.

The wider mobilisation of capital and making Ireland a centre for sustainable finance will help build the infrastructure needed for transition. But it will ultimately come back to individual corporate strategy. There is a clear need to revisit what we insure, how we insure and what we invest in is key in underpinning the long-term value proposition of insurance.

Conclusion

We are rapidly moving from a voluntary to a mandatory system of sustainability checks and balances in the insurance sector. We need to ensure that our communities, our systems and our sector as a whole do the same. I’ve identified the four mandates as vectors because we need to give both a size and a direction to our climate efforts. The clearest of these vectors are those articulating Net-Zero by 2050.

These commitments bring with them a range of actions and activities that require vector-based consideration.

All of the vectors we have identified need immediate action. Of all of these, the vector on net zero is the most important. Where a vector is best described in terms of velocity – speed in a given direction – the pace of change is critical and the scale of change is known. The velocity of our transition to net-zero is the critical vector that requires paramount attention.