The EU Green Deal will have a huge impact on business decisions and directives for the insurance sector. It requires a fresh way of thinking and operating; it’s about adopting an outside in, inside out approach, which in many cases will involve a fundamental shift in senior decision-making.

With a new report date on the horizon, let’s look closer at the requirements set out for each of the 3 key regulations, namely The Taxonomy Regulation, The Non-Financial Reporting Directive and The Sustainable Finance Disclosure Regulation.

The EU taxonomy

- This is a classification system providing companies, investors and financial market with definitions of what can be considered environmentally sustainable.

- It underpins the EU efforts to deliver capital on scale to finance the EU Green Deal.

- It’s a living document, where environmental objectives and technical standards are continually updated.

- It introduces new measures such as the green investment and green premium ratios.

The Non-Financial Reporting Directive (NFRD)

- NFRD is due to be replaced by the CSRD.

- From 2024, this will require an estimated 50,000 companies in the EU to publish sustainability information on a phased basis with small and noncomplex credit institutions and for captive insurance undertakings (reporting in 2027 on 2026 data).

- Companies will now be required to report using the Double materiality concept (the impact of Sustainability risk including climate change on the company + Companies’ impact on society and environment).

- Companies will need to use a new set of sustainability reporting standards, which are being developed by the European Financial Reporting Advisory Group (EFRAG).

- In addition, companies will need to provide information about the upstream and downstream value chain and incorporate a wider stakeholder group.

The Sustainable Finance Disclosure Regulation (SFDR)

- SFDR lays down sustainability disclosure obligations to integrate sustainability in all investment processes and for financial products that pursue the objective of sustainable investments.

- Applies to financial market participants and financial advisors in the EU along with non-EU participants who conduct business, sell products or sub-manage EU assets or funds within the EU.

- From the 1st of January 2023 the Regulatory Technical Standards (RTS) level2 are due to come into effect and are composed of the RTS text and five separate annexes.

- The RTS text runs across 5 chapters with general disclosure rules (Chapter I), PAI reporting at FMP level (Chapter II), pre-contractual disclosures for Art. 8 and Art. 9 SFDR Products (Chapter III), website disclosures for such products (Chapter IV) and periodic disclosures for such products (Chapter V). Products are now set out directly in the respective Templates which should help FMPS.

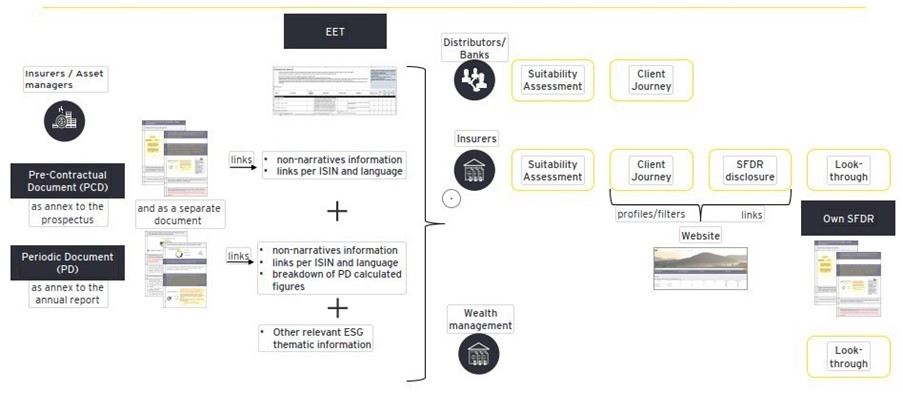

SFDR requirements through the distribution value chain (example)

How can insurance firms transition to this new model?

It’s all about gathering, refining, organising and producing the relevant data to so that it is in the correct format and is usable in terms of meeting both the regulatory -and the customers’ – needs and disclosing it in the correct manner.

Annex 1 contains the requirement to perform calculations from GHG to carbon footprints through to inefficient real estate assets using predefined formulas laid out in the annex.

Data needs to be collected at least on a quarterly basis, FMPs which have not yet started the respective data collection projects will therefore need to move extremely quickly.

The collection of PAI indicator data is also one of the main elements of the “Do No Significant Harm (DNSH)” analysis for sustainable investments and it may be difficult to qualify investments as “sustainable investments” if no data on PAI indicators is available.

Website disclosures need also to be re-examined as Article 10 requires the information to be in a separate section titled, ‘Sustainability-related disclosures’, and published in the same part of the firm’s website as the other information relating to the financial product, including marketing communications.

Navigating complex and varied requirements

Sustainable finance rules and regulations are in essence the building blocks of one single package, spread out across different areas of law. At EY, we are working with clients to navigate these new directives. Advising our insurance clients to adopt unified thinking in terms of dealing with the preparation of these complex requirements as one body of work.

- Embed climate, environmental and social factors into strategy, governance, risk management and disclosure.

- Build up capacity and capability early, employ a cross functional team which eliminates gap risk and underpins the firm wide approach.

- Maintain regulatory dialogue and engagement.

- Data – Map what you have and identify what you need, create data vaults and data enhancement capabilities.

- Create a robust framework overlayed with a flexible disclosure architecture which is forward looking and can incorporate both new regulation and iterations to the existing regulatory framework including assurance and internal audit capabilities.

If you would like more information on how EY’s team of experts can help, please get in touch.