In brief

- Irish SMEs have been profoundly affected by the pandemic. 54% are planning considerable changes to their business model with over a half of those who borrowed money over the last 18 months worried about repayment.

- There is real opportunity for Irish banks to stay ahead of the growing competition if they can provide a seamless digital experience and deliver timely access to credit.

- Banks can also drive new revenue streams by addressing the changing needs of SMEs. This can be achieved by embracing digital ecosystems and optimising their relationship management model.

SME disruption post-pandemic and what it means for FS providers

SMEs around the world have been reassessing their operations in the wake of COVID-19 with Irish businesses significantly impacted by the pandemic.

In a recent global EY survey, 54% of Irish respondents said they were planning considerable changes to their business models, driven by the dual impacts of Brexit and COVID-19. These disruptions coupled with accelerated levels of digital adoption, means that SMEs are expecting more from their financial service providers.

While banks remain the most trusted sources of finance and support, three out of ten SMEs said they were likely to switch providers. Competing providers are no longer limited to high street banks. Industry convergence – and the erosion of barriers to entry mean banks have increasing competition with 41% of Irish SMEs choosing a non-traditional bank as their primary financial institution.

The opportunties for Irish banks

Based on our comprehensive research, there are four clear opportunities for Irish banks to transform SME banking and better serve these customers in a post-pandemic world.

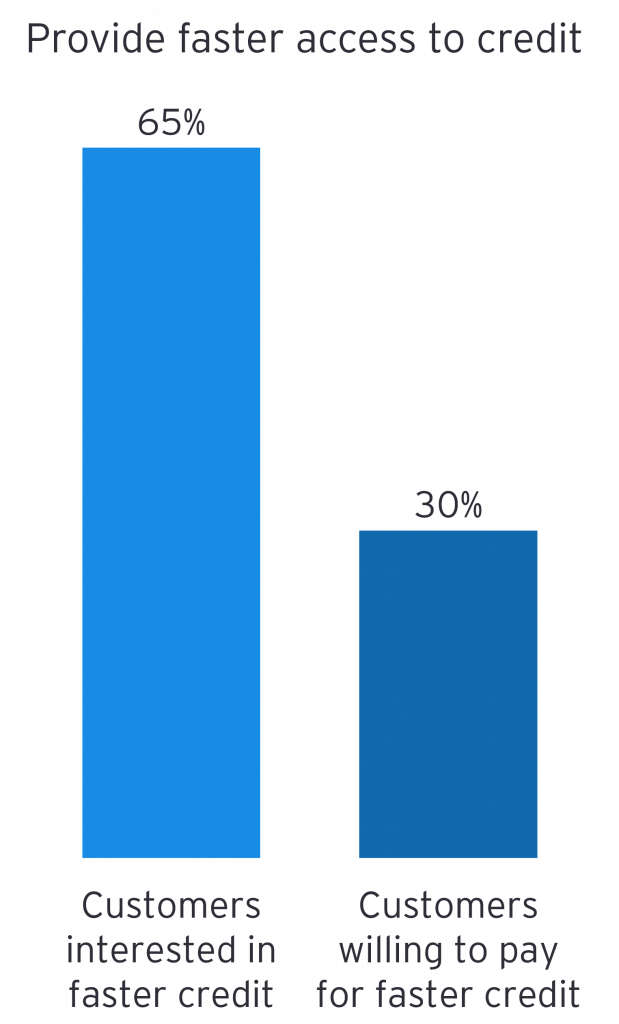

1. Provide faster access to credit

Fast access to credit in times of volatility is critical for SMEs. The pandemic underlined SME’s frustration with the speed of access to credit from their financial service provider. A third of Irish SMEs were willing to pay additional service fees to enable faster credit, compared to the global average of 20%.

The study’s findings highlight the importance of putting quantifiable parameters on what is an acceptable amount of time for the provision of credit.

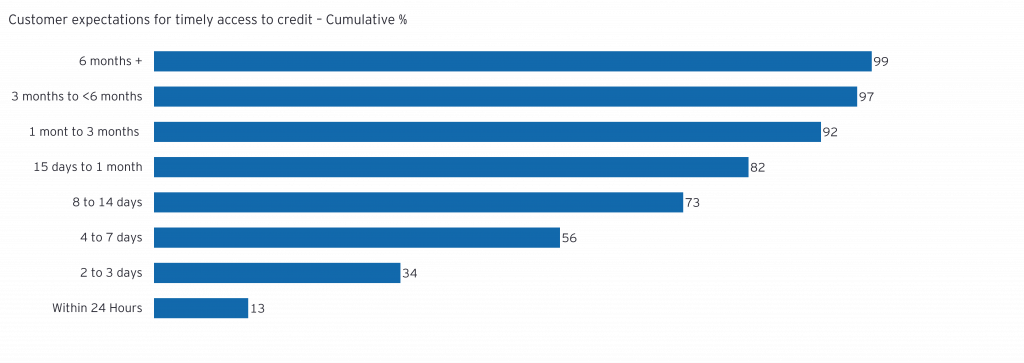

A more extensive look at the data indicates a two-tiered set of expectations across the Irish SME base. Only 34% of customers typically need access to the required funds within three days. 56% of SMEs are satisfied with access to credit within four days.

Credit risk is a key concern for both SMEs and their financial providers. In the latest EY/IIF Global Bank Risk Survey, 98% of CROs cited credit risk as their number one concern over the next 12 months.

Of the 50% of SMEs that borrowed money to support their business during the pandemic, 54% of respondents said that they are moderately, very or extremely concerned about repaying it. If the Irish economy experiences an uneven, prolonged recovery, or adverse economic conditions prevail, SME credit issues are likely to grow. It is imperative the wider economy that access to credit is provided to meet the requirements of the business.

To mitigate the risk of SMEs getting into repayment difficulty, banks should gain a better understanding of their customer’s credit health. They can do this by embracing the opportunity of open banking combined with emerging technology, e.g. Artificial Intelligence (AI), and leveraging open banking technology to access data direct from external sources. To be truly effective, addressing underlying data quality constraints is essential.

2. Accelerate transformation of the customer experience

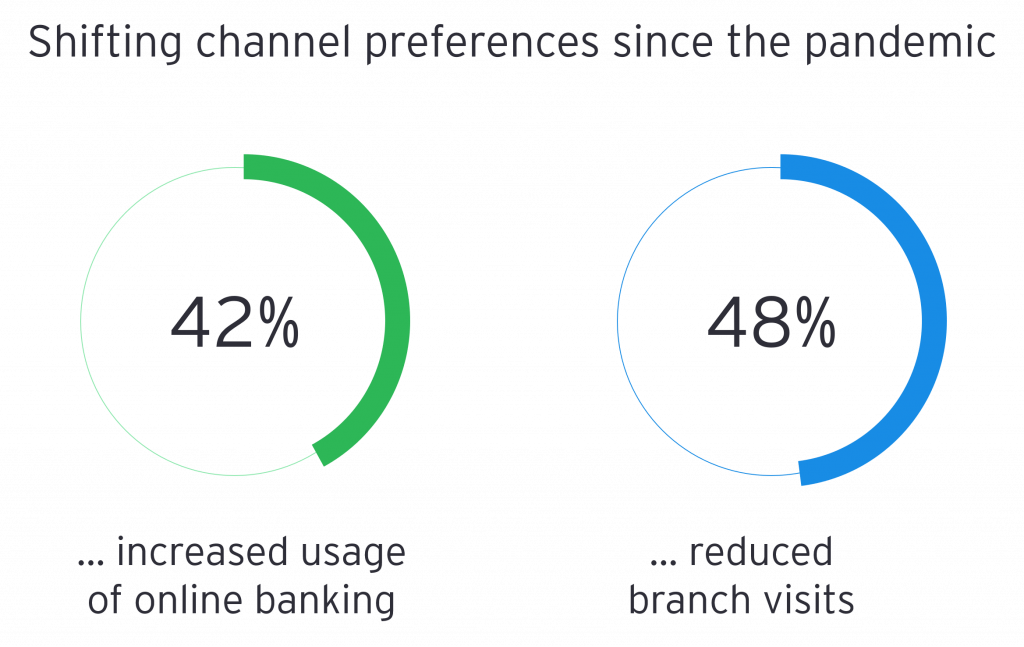

Demand for digital dramatically increased during the pandemic with 42% of Irish SME respondents increasing their use of online banking services. At the same time, 48% reduced their visits to branches and offices compared to 38% globally.

Despite the acceleration of digital adoption, only 54% said their current financial services institution offered a streamlined digital experience, compared to 62% of global respondents. As the adoption of open application programming interfaces (APIs) and platform-based services increases, end-to-end frictionless digital experiences, such as onboarding are becoming industry standards.

The potential to partner with FinTechs to address streamlined operational processes and accelerate market propositions without having to build and maintain in-house technology is an attractive opportunity. The digitisation of labour-intensive processes and the revenue increase resulting from enhanced customer experience can directly improve Cost to Income ratio challenges.

3. Unlock new revenue streams via the ecosystem opportunity

As outlined in a recent EY article, digital ecosystems – including embedded finance – are the future of banking. They are new propositions and innovative customer experiences built on collaborations and partnerships. Developing an ecosystem offering, and grouping services beyond banking, can help traditional banks respond to increasing market competition and profitability challenges.

Embracing ecosystems is moving from being an opportunistic approach to becoming a revenue-generating strategic competitive imperative. Irish banks that seize this opportunity can unlock a larger addressable wallet.

A recent report EY developed with the BPFI showed that Irish retail banks are overly reliant on interest income. Net interest income accounts for c. 80% of operating income compared to c. 54% in the EU banking sector. Building or participating in digital ecosystems which address SME needs can help address this dependency and generate new non-interest revenue streams.

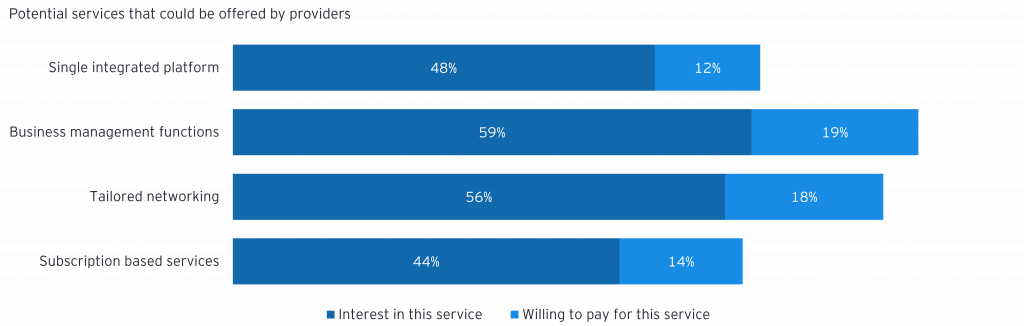

The survey identified several services that Irish SMEs would be willing to pay for:

Single integrated platform

70% of Irish SMEs use more than one financial institution with 7% using more than ten which may indicate that primary providers are not providing a full set of needs for their customers. In the future, the convenience of a unified experience or a single interface for all banking needs will become a baseline expectation. New Fintech providers have entered the market, working on service aggregation with banks looking to be early adopters of this growing trend.

Business management functions

59% of Irish SMEs are looking for help with non-core activities, especially around key growth milestones. 18% of SMEs would be prepared to pay for Banks to provide additional business supports such as legal, advisory, risk management and other management capabilities in a coherent, accessible manner.

Tailored networking

56% of Irish SMEs expect their banking providers to understand what they need to advance their business strategies and connect them to growth opportunities. Banks should be looking to connect like-minded and complementary clients with curated network of third-party service providers. Of the 18% who said they are willing to access this service from their bank, all were willing to pay for the service.

Tailored data service

Over a half of respondents indicated they would be prepared to pay for a data exchange with banks which would enable personalised and richer insights into their business.

Subscription-based services

Just as consumers have grown comfortable with subscription models, so too Irish SMEs want the ability to add or remove products and services quickly. Banks should provide customised solutions, with interchangeable products driven by business flows and forecasts.

4. Transform relationship management models to deliver brilliant basics and trusted relationships

Expectations from Irish SMEs of their financial services provider/relationship manager (RM) are similar to global trends. 69% want the basics such as payments and access to credit facilities done brilliantly before any further value-add services are offered. However once banks are providing these basic services well, 21% would welcome a tailored trusted advisor service offered by providers for a fee.

Banks can look to support the delivery of brilliant basics through the implementation of an augmented RM model which supports RMs solving their clients everyday needs. This has been successfully deployed elsewhere with additional functionality such as payments, same day overdrafts and cash flow insights with a growing roadmap of functionality.

Implementation of this type of digital tooling can free up capacity for the RMs to provide the value-added, trusted advisor role that SMEs want. This also provides banks with another option to diversify their revenue streams away from Net Interest Income.

Real-time, AI-driven and contextually relevant insights will enable hyper-personalisation and help banks provide greater service at a lower cost. Combining this with a localised premium RM model for select customers could be a compelling offering in the Irish market.

Conclusion

The pandemic has had a profound impact on the SME landscape. As they respond by evolving their business models, Irish banks must focus on the real needs of SMEs as they themselves transform in the post-pandemic era.

Once banks get the basics right, there is an exciting opportunity for them to diversify their revenue streams by providing a seamless digital experience, embracing ecosystems and transforming the relationship manager model. Banks who embrace the challenge set by their SMEs will differentiate themselves from their peers and set them up for success.

Banking experiences and expectations

The Voice of the SME

Our latest SME Survey shows that small and medium-sized enterprises (SMEs) are often the hardest hit when crises emerge, and the COVID-19 pandemic has been no exception. The insights we gathered from over 5,600 business leaders across the globe draw five clear steps for banks to follow in order to better serve SMEs in a post-pandemic world.

Read the Global SME Survey 2021 here

Contact Us

We know there are a huge number of considerations for financial institutions as they look to support their SME clients and build value for the future. Contact us today to discuss the SME banking opportunities for your organisation.

Oliver Pugh, FS Partner, Consulting

Contact Us